In this listicle roundup, you will find a clear picture of how enterprises are actually adopting large language models, based on numbers rather than opinions. The statistics in this article show where LLMs are already in use, how fast adoption is accelerating, which models and deployment methods enterprises prefer, and where real value is being created or delayed. This is not a future-looking piece. Every data point reflects current enterprise behavior, spending patterns, and operational outcomes.

We collect data from trusted online sources, including enterprise surveys, analyst reports, and official vendor disclosures. For transparency, all source URLs are attached at the end of the article so you can review the original research and validate the findings yourself.

LLMs are becoming core infrastructure. Hire pre-vetted AI engineers from Index.dev who know how to deploy, scale, and govern them in production.

Key Takeaways: LLM Enterprise Adoption

- Enterprise LLMs are moving from tools to infrastructure, with the market set to grow 10× from $6.7 billion to $71.1billion by 2034.

- Adoption is accelerating faster than cloud or mobile, jumping from under 5% in 2023 to over 80% by 2026.

- LLM adoption is enterprise-led, with 78% of usage coming from large organizations, not startups or SMBs.

- The LLM market is already concentrated, with seven vendors accounting for nearly 80% of market share, shaping standards and pricing.

- Cloud has become the default LLM operating layer, powering over 40% of enterprise deployments.

- Enterprises favor scale over specialization today, with general-purpose LLMs generating more than half of all revenue.

- Accuracy and compliance are becoming the next battleground, as domain-specific LLMs grow at 38%+ CAGR, the fastest in the market.

- Customer support is the first clear LLM win, capturing over 30% of enterprise LLM revenue due to measurable ROI.

- Enterprise spending is no longer cautious, with 72% planning higher investment and 40% budgeting over $250K.

- Despite heavy adoption, execution lags badly, as only 36% have scaled GenAI and just 13% see enterprise-wide impact.

Market Size, Growth, and Industry Structure

When you look at market size, growth rate, and vendor concentration, you are trying to understand how permanent enterprise LLM adoption really is. These numbers tell you whether LLMs are being treated as short-term innovation tools or as long-term business infrastructure similar to cloud platforms or ERP systems.

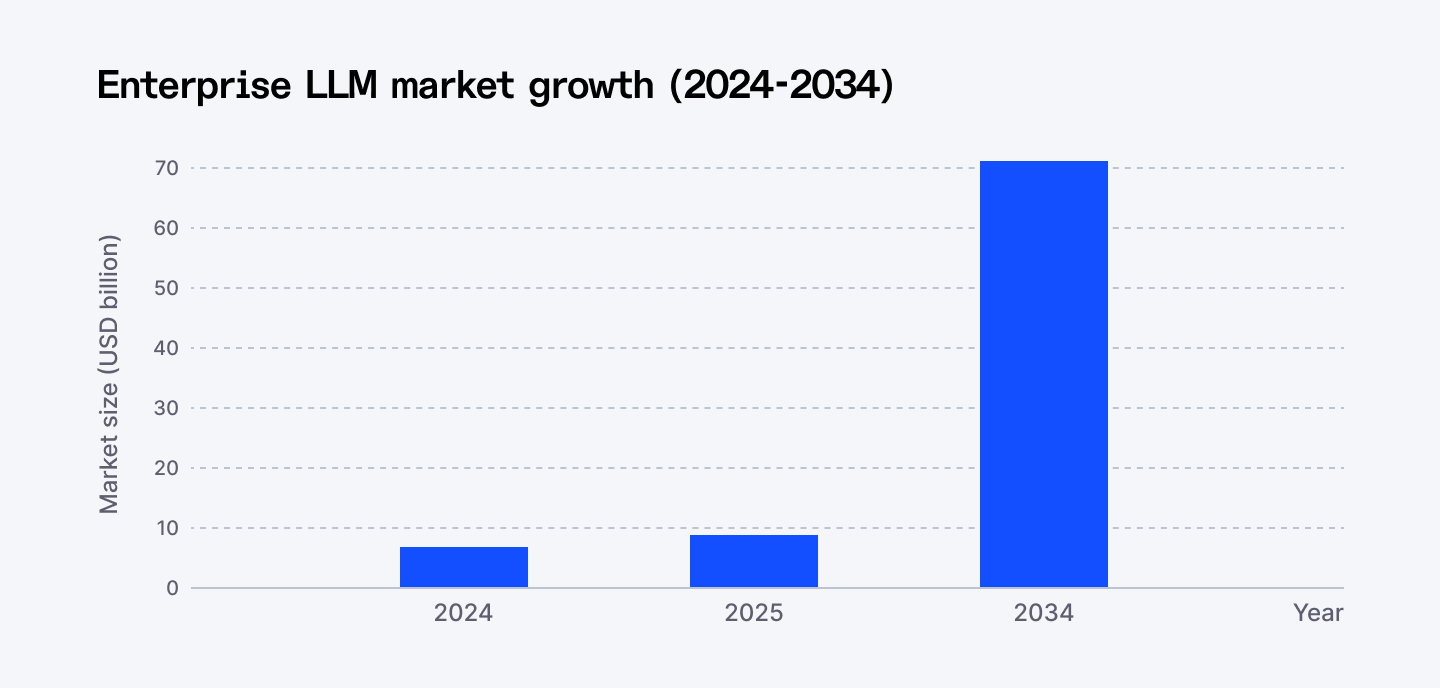

- The enterprise LLM market was valued at $6.7 billion in 2024 and is expected to grow from $8.8 billion in 2025 to $71.1 billion by 2034, at a 26.1% CAGR, indicating sustained long-term enterprise investment rather than short-term pilot spending.

- Microsoft, OpenAI, Anthropic, Google, AWS, Cohere, and AI21 Labs together control around 79% of the market, indicating that enterprise adoption is concentrated among a small group of vendors with proven scale, security, and integration capabilities.

- Large enterprises account for 78% of the LLM market share, indicating that most adoption is occurring within complex organizations with high data volumes and multi-department workflows.

- The software segment leads the market and is forecast to grow at a 28.2% CAGR from 2025 to 2034, indicating that enterprises primarily spend on model access, platforms, and orchestration layers rather than on hardware.

- North America holds a 32.9% market share, driven by stronger cloud infrastructure, higher enterprise AI readiness, and earlier adoption across industries.

Enterprise Adoption Momentum Across Private and Public Sectors

Adoption momentum helps you judge how quickly LLMs are moving from interest into everyday operations. When both private enterprises and public agencies report active use and measurable outcomes, it signals that reliability and governance concerns are being addressed in practice.

- More than 87% of Brazilian business leaders plan to maintain or increase AI investment in 2025, while 90% of large companies already operate at least one AI use case, showing strong private-sector commitment.

- Public agencies using chatbots and document analysis doubled approval processing throughput and reduced homologation time by 85%, demonstrating measurable operational efficiency.

- By 2026, over 80% of enterprises are expected to have deployed generative AI APIs or models, up from less than 5% in 2023, reflecting a rapid shift from experimentation to deployment.

- More than 80% of enterprises are expected to deploy generative AI applications or APIs by 2026, reinforcing the scale of adoption across organizations.

- 67% of organizations already use generative AI products powered by LLMs, confirming that adoption is now mainstream rather than early-stage.

Up next: See how ready different countries really are for AI and who’s falling behind in 2026.

Deployment Models and Infrastructure Choices

Infrastructure data shows you how enterprises are actually running LLMs in real environments. Deployment choices affect how fast you can scale usage, how securely data is handled, and how predictable costs remain over time. When cloud deployment dominates across multiple years, it indicates that enterprises prioritize flexibility and speed over owning infrastructure.

- Cloud-based deployment led the market with a 49% share in 2024, indicating that most enterprises prioritize scalability and speed over owning infrastructure.

- Cloud deployment continued to dominate in 2025, with a 41.74% revenue share, confirming that cloud remains the default choice for enterprise LLM rollouts.

- International API customer growth exceeded 70% in the last six months, with Japan having the largest number of corporate API customers outside the US, demonstrating global enterprise adoption.

- 63% of enterprises use paid or enterprise LLM versions, while 17% rely on free tiers, indicating that most organizations run LLMs in production rather than in testing environments.

Model Types and Architecture Trends

Model and architecture trends help you understand how enterprises manage accuracy, compliance, and reuse at scale. These numbers show whether companies prefer flexible models that serve many teams or specialized models built for specific workflows.

- General-purpose LLMs accounted for 54% of total enterprise LLM revenue in 2024, indicating that most companies standardize on models that support multiple internal and external use cases.

- Domain-specific LLMs are projected to grow at a CAGR exceeding 38% from 2025 to 2033, driven by rising enterprise demand for greater accuracy and regulatory alignment.

- Retrieval Augmented Generation models dominated with a 38.41% revenue share in 2025, reflecting the enterprise's focus on accuracy, auditability, and context-aware responses.

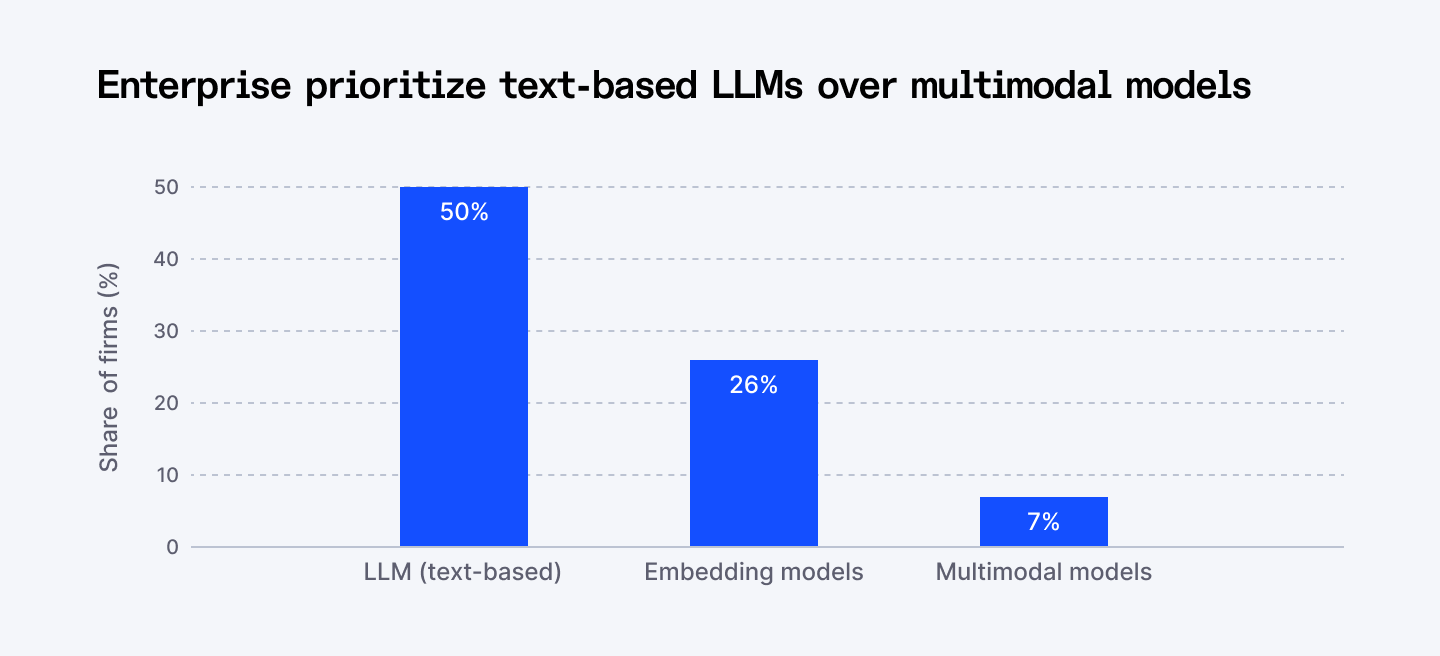

- As of 2024, over 50% of firms planned to use LLMs such as LLaMA, 26% used embedding models, and only 7% planned to use multimodal models, indicating a strong text-first adoption pattern.

- General-purpose LLMs accounted for 41.6% of global enterprise revenue, driven by demand for automation across customer service, content creation, and data analysis.

Vendor and Model Usage Patterns

Usage patterns reveal which LLM providers enterprises actually trust with internal workflows and customer-facing systems. These figures help you understand how competitive the landscape is, how quickly new models gain acceptance, and whether enterprises are standardizing or diversifying their AI stacks.

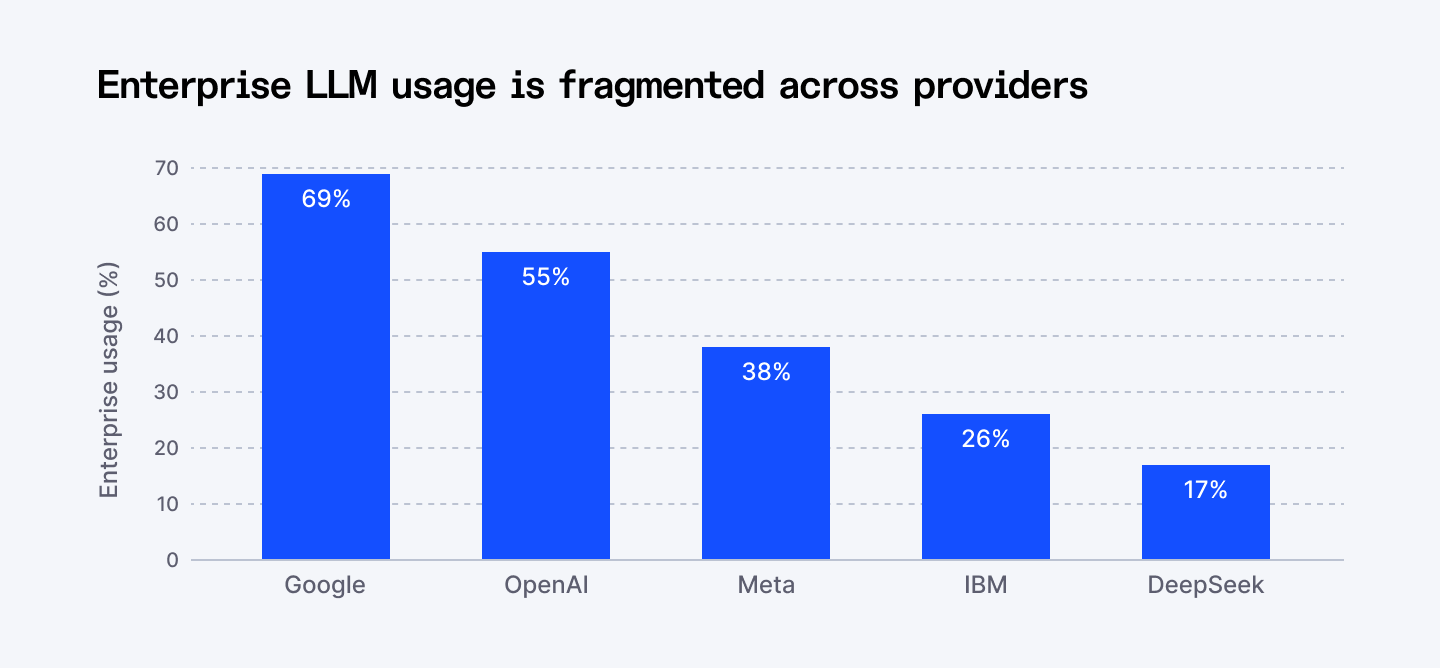

- In Q1 2025, 69% of enterprises reported using Google models, compared to 55% using OpenAI models, indicating shifting enterprise usage patterns.

- DeepSeek reached 17% adoption in 2025, with 80% of respondents reporting they are comfortable using it in the workplace, indicating early but growing acceptance.

- Enterprise model usage includes 69% Google, 55% OpenAI, 38% Meta, 26% IBM, and 17% DeepSeek, indicating that many organizations use multiple models simultaneously.

- OpenAI serves over 1 million business customers and more than 7 million ChatGPT workplace seats, with enterprise seats growing 9x year over year, demonstrating rapid enterprise-scale growth.

- Weekly users of Custom GPTs and Projects increased 19 times year-to-date, with around 20% of enterprise messages processed through them, indicating rising customization.

Enterprise Use Cases and Functional Adoption

Use case data helps you connect LLM adoption to concrete business activity. These numbers show where enterprises see immediate value and how usage spreads across departments over time. Early focus areas such as customer support and developer productivity reflect functions with high volume, repeatable tasks, and clear ROI.

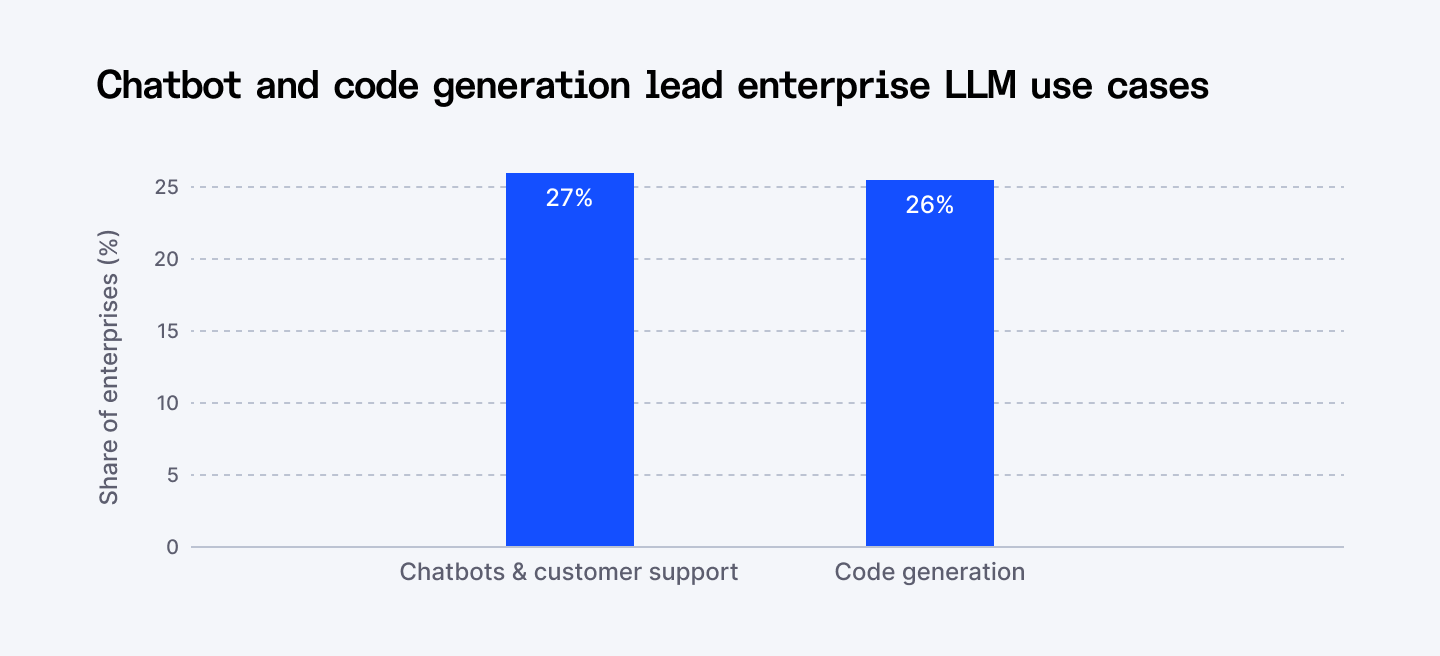

- AI-powered chatbots and customer support are the primary use cases for 27% of enterprises, followed by code generation at 26%, indicating a focus on efficiency and productivity.

- 20% of organizations plan to use information extraction as their first LLM use case, followed by training and testing (18%), content generation (17%), and document review (15%).

- 48% of organizations planning LLM adoption expect to enhance customer service and support, rising to 66% among leaders who feel very prepared.

- Customer support dominated the market with a 32.48% revenue share in 2025, driven by rising volumes of customer interactions.

- Healthcare is expected to grow by 28.12%, driven by clinical documentation, medical coding, and decision-support systems.

Investment Levels and Budget Commitment

Investment figures tell you whether enterprises are experimenting or fully committing. For you, these numbers help benchmark your own investment decisions and understand how aggressively leading organizations are funding LLM adoption across technology, people, and process change.

- 72% of companies plan to increase investment in generative LLMs, and 40% expect to spend more than $250,000, indicating enterprise-wide deployment plans.

- Future-built companies plan to spend 26% more on IT and allocate up to 64% more of their IT budgets to AI, expecting stronger revenue growth and cost reductions.

- Only 5% of companies are classified as future-built, while 35% are actively scaling AI, showing uneven maturity across enterprises.

Productivity Impact and Measured Business Value

Productivity data answers a practical question. What do enterprises actually gain from using LLMs day to day? Time savings, usage intensity, and workflow integration metrics translate adoption into measurable outcomes. These numbers help you understand which roles benefit most and how deeply LLMs must be embedded into workflows to deliver meaningful returns.

- 46% of organizations say the biggest impact of generative AI is improved productivity and innovation.

- ChatGPT Enterprise users save 40 to 60 minutes per active day, with data science, engineering, and communications roles saving 60 to 80 minutes per day.

- Integrating LLM copilots into office automation tools yields 27-74% time savings without reducing output quality.

- Frontier firms generate twice as many messages per seat and seven times as many to GPTs as median enterprises, indicating deeper integration.

Organizational Readiness and Scaling Gaps

Readiness metrics explain why adoption does not always lead to impact. Even when tools are available, scaling depends on skills, integration, and change management. These figures help you see where enterprises struggle most, whether in preparation, usage depth, or enterprise-wide rollout.

- Only 36% of executives say their organization has scaled generative AI, and just 13% report a significant enterprise-level impact.

- Only 30% of senior technologists feel well-prepared to adopt LLMs, even though 90% believe fine-tuned LLMs would deliver value.

- Among monthly active users, 19% have never used data analysis, 14% have never used reasoning, and 12% have never used search, showing underutilization.

Security, Governance, and Provider Selection

Security and governance data show why enterprise LLM adoption often slows after initial pilots. Concerns around data privacy, regulatory compliance, and model reliability shape both provider selection and deployment scope. These numbers help you understand which risks dominate decision-making and why addressing trust early is critical.

- 31% of enterprises rank security and data privacy compliance as the top factor when selecting an LLM provider.

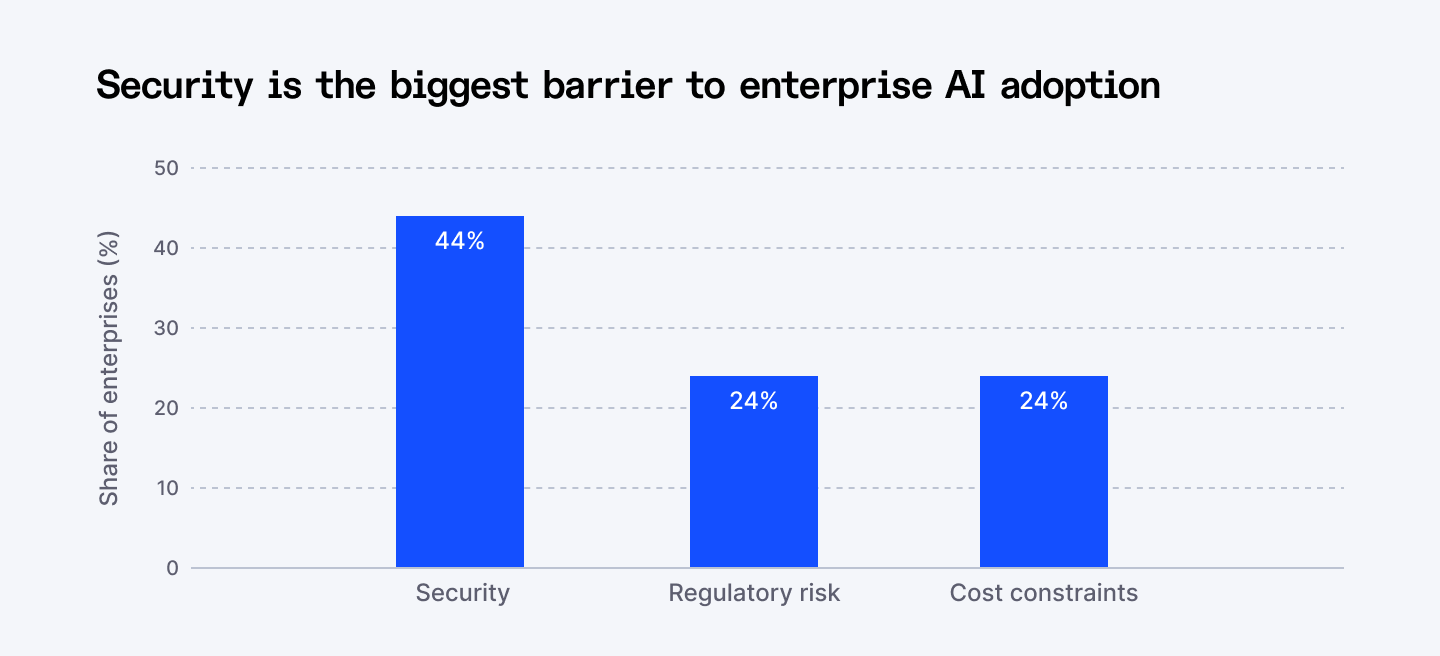

- 44% identify security as the greatest barrier to adoption, followed by regulatory risk (24%) and cost constraints (24%).

- Organizations that operationalize AI transparency, trust, and security achieve 50% better adoption and business outcomes.

Workforce Sentiment and Leadership Focus

Workforce and leadership sentiment influence the extent to which LLMs are adopted. When employees view AI as supportive rather than threatening, usage expands faster and more naturally. Leadership attention also signals strategic intent, shaping funding and prioritization. In this section, you will understand cultural readiness, internal acceptance, and how executive focus accelerates or limits adoption.

- Only 1 in 10 developers believe LLMs will lead to layoffs, while 82% are optimistic about GenAI’s impact on their work.

- 49% of executives expect generative AI tools to be partially accessible to employees over the next 3 years.

- Executive discussions around agentic AI increased 41 times after the release of ChatGPT, showing sharp leadership focus.

Emerging Value and Advanced AI Trends

Advanced trends show where enterprise AI value is heading next. Usage growth data shows how quickly LLMs become part of everyday work once adoption takes hold.

- Agentic AI already accounts for 17% of total AI value and is expected to double by 2028.

- 70% of AI’s potential value is concentrated in core business functions such as R&D, innovation, and digital marketing.

- Weekly enterprise ChatGPT messages grew 8 times since November 2024, with the average worker sending 30% more messages year over year.

- Codex enterprise usage doubled, with weekly active users increasing by about 50%, indicating growing AI-assisted development.

Read next: Discover where AI growth is accelerating worldwide and what it means for businesses this year.

Final Words

The statistics in this roundup show clear patterns. Enterprise LLM adoption is advancing faster than most organizations can operationalize it. While market size, usage rates, and investment levels are rising sharply, scaling, governance, and workforce readiness are lagging. This gap between adoption and impact is where most enterprise risk and opportunity now sit.

You can use these data points to benchmark your organization’s position, validate budget decisions, and prioritize next steps. Focus first on use cases with proven ROI, align security and compliance early, and measure productivity impact consistently. The next phase of enterprise LLM adoption will be defined less by access to models and more by execution discipline.

➡︎ The stats don't lie: 80% adoption but only 13% see real impact. The difference? Engineering talent that can deploy and scale LLMs in production. Index.dev connects you with senior developers who've moved enterprise AI from pilot to production, the rare engineers who close the execution gap revealed in these statistics.

➡︎ Want to go deeper into where AI is really headed? Explore more Index.dev insights on AI literacy and what it means in 2026, how AI is reshaping application and cloud development, and which industries are closest to a real AI tipping point. You can also dig into practical perspectives on why forward-deployed engineers matter, plus hands-on model comparisons that break down DeepSeek versus ChatGPT, how it stacks up against Claude, and which open-source Chinese LLMs are gaining serious traction.

FAQs

How widely are enterprises adopting large language models?

Around 67% of organizations already use LLM-powered generative AI, and over 80% of enterprises are expected to deploy GenAI applications or APIs by 2026. Adoption has jumped from less than 5% in 2023, showing that LLMs are moving rapidly from experimentation into production use across industries and regions.

What is the current and future market size of enterprise LLMs?

The enterprise LLM market was valued at $6.7 billion in 2024 and is projected to reach $71.1 billion by 2034. The market is expected to grow from $8.8 billion in 2025 at a CAGR of 26.1%, reflecting sustained enterprise investment rather than short-term AI experimentation.

Which enterprises are driving most LLM adoption?

Large enterprises account for 78% of the total enterprise LLM market share. This shows that adoption is primarily driven by organizations with complex operations, large datasets, and multiple business functions, rather than small companies or early-stage startups testing isolated AI use cases.

What are the most common enterprise use cases for LLMs?

AI-powered chatbots and customer support represent 27% of enterprise LLM use cases and over 32% of market revenue. Code generation follows closely at 26%, with additional use cases including information extraction, content generation, and document review, all focused on productivity and operational efficiency.

Which LLM deployment model do enterprises prefer?

Cloud-based LLM deployment leads the market with a 49% share in 2024 and 41.74% in 2025. Enterprises favor cloud models for faster deployment, elastic scaling, and centralized access, while hybrid and on-premise deployments remain important for regulated and compliance-heavy environments.

Data Sources

- https://www.gminsights.com/industry-analysis/enterprise-llm-market

- https://konghq.com/resources/reports/generative-ai-enterprise-trends-2025

- https://www.gartner.com/en/newsroom/press-releases/2023-10-11-gartner-says-more-than-80-%-of-enterprises-will-have-used-generative-ai-apis-or-deployed-generative-ai-enabled-applications-by-2026#:~:text=AI%20TRiSM%20is%20an%20important,business%20goals%20and%20user%20acceptance.

- https://assets.prd.mktg.konghq.com/files/2025/06/685c3aec-kong-2025-report---genai-in-the-enterprise.pdf

- https://www.accenture.com/content/dam/accenture/final/accenture-com/document-3/Accenture-Tech-Vision-2025.pdf#zoom=40

- https://vertesiahq.com/hubfs/Documents/Vertesia-Censuswide-Survey-Report.pdf

- https://cdn.openai.com/pdf/7ef17d82-96bf-4dd1-9df2-228f7f377a29/the-state-of-enterprise-ai_2025-report.pdf

- https://www.bcg.com/press/30september2025-ai-leaders-outpace-laggards-revenue-growth-cost-savings#:~:text=Further%2C%20BCG's%20analysis%20shows%20that,and%201.6x%20EBIT%20margin.&text=A%20key%20driver%20of%20this,the%20rise%20of%20agentic%20AI.

- https://www.bcg.com/publications/2025/are-you-generating-value-from-ai-the-widening-gap

- https://www.managementsolutions.com/sites/default/files/minisite/static/72b0015f-39c9-4a52-ba63-872c115bfbd0/llm/pdf/rise-of-llm.pdf

- https://www.statista.com/statistics/1485176/choice-of-llm-models-for-commercial-deployment-global/

- https://market.us/report/large-language-model-llm-market/

- https://www.grandviewresearch.com/industry-analysis/enterprise-llm-market-report

- https://straitsresearch.com/report/enterprise-llm-market